Rigged: you be the judge

The secret history of interest rate rigging

This is a free interactive timeline for readers of 'Rigged' by Andy Verity.

It contains audio recordings that the authorities on both sides of the Atlantic didn’t want you, the public, to hear.

Also embedded are links to copies of emails, confidential documents and contemporaneous news articles that reveal a secret history spanning 16 years: an unsettling true story of a high-level cover-up on both sides of the Atlantic followed by a series of miscarriages of justice in the UK and US.

Much of this evidence has never been shown to Congress nor to the UK Parliament. Some of the most powerful evidence was never put before juries in nine criminal trials in New York and London.

To get to know this story for free, you can listen here to The Lowball Tapes, a BBC Radio 4 investigative podcast series broadcast in 2022 and shortlisted for three awards.

The book, which contains much exclusive information in addition to what is set out below, including the personal stories of traders wrongfully prosecuted for ‘manipulating’ interest rates, can be purchased here.

This is the latest of many updates to this timeline to be published in the coming weeks, eventually bringing it right up to the present day. The new material is at the bottom of the timeline, now covering the explosion of public outrage that greeted the Barclays fines - the first official confirmation that bankers had behaved so badly they should be fined by the US and UK authorities. But hold on - which bankers - and what for? The banks’ lawyers - and the top bosses overseeing them - were the ones who decided the answers to that question. They also supplied the prosecutors with the evidence with which to prosecute them….

I’m open to any comments on this timeline from any source, either here on Substack or via direct message to my Twitter account. I’ll also update it if I learn something editorially relevant and new to me.

Click on the links and the embedded audio below to see and hear evidence of the cover-up, followed by what prosecuted traders and brokers say was a stitch-up.

Could that be true?

You be the judge:

1969

To set interest rates on large loans, Greek banker Minos Zombanakis invents a formula that reflects banks’ shifting cost of funds. The first is an $80m loan to the Shah of Iran.

1970s

The formula, now named ‘Libor’ (the London Interbank Offered Rate) is used with increasing frequency to set interest rates for large offshore loans in US dollars.

January 1986

In response to a Bank of England request, the British Bankers Association (BBA) launches the brand ‘BBA Libor’. It issues instructions to 16 banks to publish a daily estimate of what interest rate they would pay to borrow a large sum of cash from other banks.

{kind=link}

1986 to 2012

Traders on the cash desks of 16 banks on the Libor ‘panel’ answer the Libor question each working day: at what interest rate could they borrow cash in reasonable size at 11am?

They select the rate they will publish from the narrow range of interest rates on offer in the market at which they could borrow cash (eg money brokers tell them there are offers at 3.43%, 3.45% and 3.44%; they publish any one of those three).

With nothing to choose between that range of accurate answers to the Libor question, traders on cash desks check each day with colleagues on derivatives desks (who trade financial instruments that go up or down in price linked to Libor) whether they would prefer Libor high or low. That way the rate they select will be in keeping with a key part of their jobs - to do everything with their bank’s commercial interests in mind.

Traders in derivatives linked to Libor routinely ask their cash desk colleagues to quote their banks’ Libor estimates ‘high’ or ‘low’ to suit their bank’s commercial interests (eg trading positions):

December 1998

Euribor, the Euro Interbank Offered Rate, is published for the first time. Its founders are Helmut Konrad, then president of ACI Germany, a financial markets organisation of foreign exchange and money market traders; Jean Pierre Ravisé, president of ACI France; and Nikolaus Bömcke, then secretary general of the industry body the European Banking Federation, who drafts the code of conduct.

18 August 2005

The BBA’s John Ewan tells senior Bank of England officials of daily commercial influence on Libor. Libor is ‘some 3 to 4 basis points over the actual market rate as it’s in the interests of banks to have a higher Libor’. (No-one falls off their chair.)

{kind=link}

17 July 2007

Bear Stearns discloses that two hedge funds investing in US subprime mortgages have lost nearly all of their value.

20 July 2007

US Federal Reserve chair Ben Bernanke tells Congress that the amount of money lost on US sub-prime mortgages that aren’t being repaid could be up to $100bn.

9 August 2007

BNP Paribas announces it is freezing three hedge funds that specialised in US mortgage debt, indicating it has no way of valuing its mortgage investments. Credit crunch begins.

August 2007 - October 2009

Banks continually post Libor rates much too low to reflect the real cost of borrowing cash: lowballing.

10 August 2007

The huge, unknown scale of US mortgage losses has made banks reluctant to lend money to other banks for fear they might not get it back. Clive Jones of Lloyds tells BBA’s John Ewan no Libor is based on the definition as there are no cash offers in the market. Has the Bank of England spoken to the BBA about it?

Ewan consults other practitioners on the body that runs Libor, the Foreign Exchange and Money Markets Committee and comes back to Jones. Jones tells Ewan that Lloyds’s Libor isn’t real.

{kind=link}

14 August 2007

German bank Landesbank Hessen-Thuringen Girosentrale tells the Bank of England Libors are ‘totally distorted, 25-30 bps away from where they should be’.

{kind=link}

BoE’s Paul Tucker calls senior bankers from RBS, Barclays, HSBC, Lloyds and HBOS to a confidential meeting. They agree Libor fixings are too low and there’s a case for raising them considerably higher. In the next two days, banks hike rates by 20-25 basis points.

{kind=link}

{kind=link}

16 August 2007

The committee than runs Libor, the Foreign Exchange and Money Markets Committee discusses how banks can’t set Libor properly because there are no offers to lend cash.

20 August 2007

German bank Landesbank Baden-Wurttemberg tells the Bank of England it believes banks are manipulating Libor.

{kind=link}

Barclays head of European Collateralised Debt Obligations (investments linked to US subprime mortgages) Ed Cahill resigns.

22 August 2007

Deutsche Bank warns the Bank of England that other banks are setting Libor ‘artificially low to allay market concerns’ – a practice later called ‘lowballing’.

{kind=link}

Standard & Poor’s slashes credit ratings for two ‘structured investment vehicles’ exposed to US mortgages created by Barclays and places a third on review.

28 August 2007

Returning from holiday, Peter Johnson notices US dollar Libors are too low and corrects his rate upwards. He sends an email, ‘Draw your own conclusions about why people are going for unrealistically low Libors’, forwarded the same day to the New York Fed. (In July 2012, the email is released after Barclays Legal has redacted it, removing Johnson’s name).

29-31 August 2007

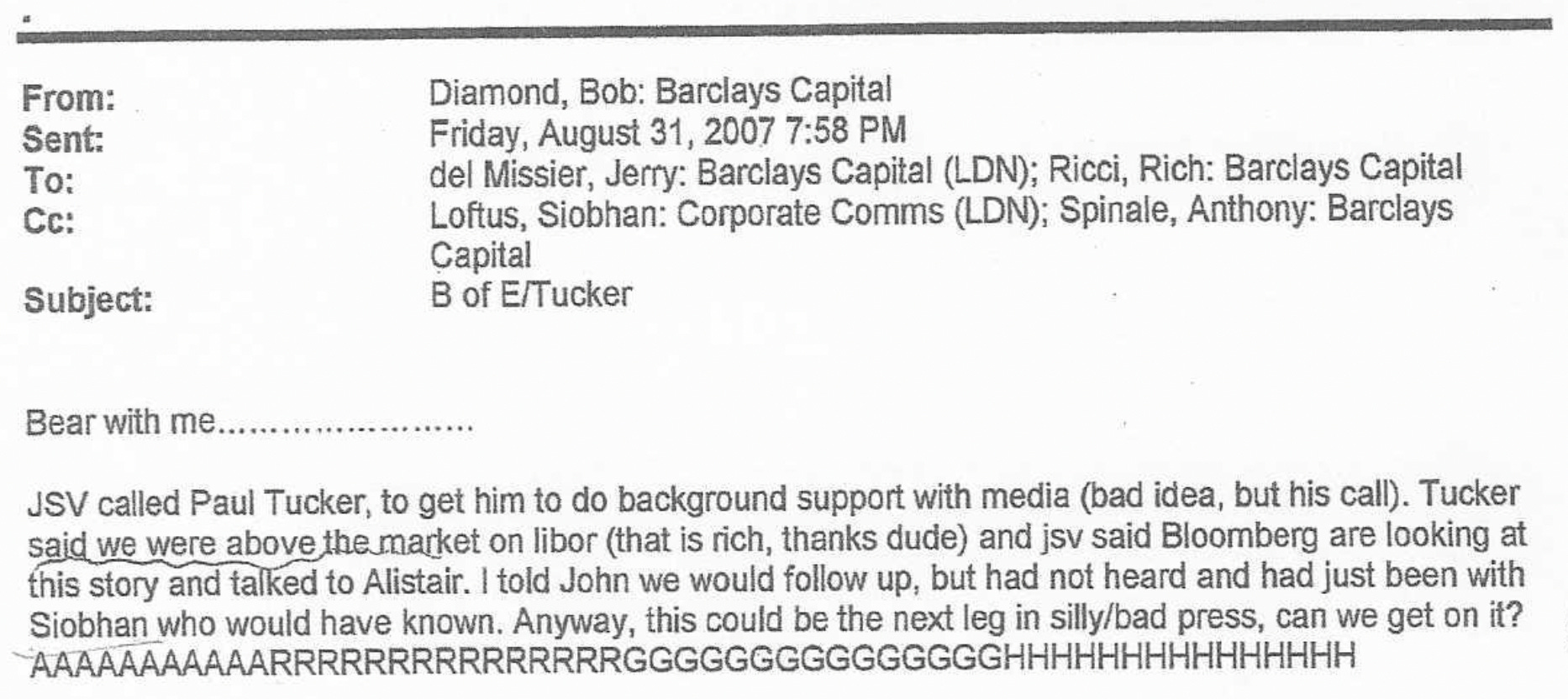

Barclays bosses Jerry del Missier, Bob Diamond and John Varley discuss negative media speculation about Barclays’ financial state with Paul Tucker, who tells Diamond that Barclays is above the market on Libor. “AAAARRRRRGGGGHHH!!!’ says Diamond privately.

{kind=link}

31 August 2007

Financial Times article ‘Anxious Market Catches Barclays Short of £1.6bn’.

1 September 2007

The last date of the indictment period covering the ‘conspiracy to defraud’ by Barclays traders as alleged at trial by the Serious Fraud Office (1 January 2005 -1 September 2007)

1 September 2007

In a Saturday phone call Tucker tells del Missier ‘you should get your Libor rates down’, according to sworn testimony to the US Department of Justice by del Missier.

3 September 2007

Bloomberg report ‘Barclays Takes a Money Market Beating’ suggests Barclays’ higher Libor rates may be further evidence that it’s in financial difficulty.

Peter Johnson (PJ) wants to raise his Libor submission to reflect the higher cost of borrowing but is instructed not to by head of group balance sheet Miles Storey, who’s received an instruction passed down by del Missier. PJ tells a colleague he’s under political pressure from senior managers to understate his Libor estimate.

13-14 September 2007

BBC’s Robert Peston reveals Northern Rock has asked for and been granted emergency liquidity assistance (cash) from the Bank of England, prompting a run on the bank.

20 September 2007

At a Barclays board meeting including then chief executive John Varley and his deputy Bob Diamond it’s agreed that finance director Chris Lucas will take the lead on Libor, with group treasurer Jonathan Stone as a conduit to Dearlove.

21 September 2007

PJ tells the Federal Reserve Bank of New York (‘the New York Fed’) about lowballing, as he tells his New York colleague Ryan Reich later that day:

September 2007 - October 2009

PJ protests other banks’ dishonestly low, inaccurate Libor submissions, trying to post higher, more honest rates. But Storey and Dearlove repeatedly pass down instructions from the board of Barclays not to stand out too far from ‘the pack’ of other banks’ published Libor estimates of the cost of borrowing, meaning he’s also lowballing.

21 November 2007

Barclays group treasurer Jonathan Stone and PJ’s immediate boss Mark Dearlove express relief that PJ’s Libor rates no longer stand out above other banks. Stone tells him he doesn’t want Barclays to have the highest submission – ‘you’ve heard Bob as well. We don’t want to be in the press. It just ain’t worth it.’

29 November 2007

PJ’s boss Mark Dearlove calls Jonathan Stone to an emergency conference call (you can listen in below) with head of balance sheet management Miles Storey, PJ and Colin Bermingham. Fearing a ‘shitstorm’ if PJ posts what he thinks is a fair Libor rate – 5.50% - Dearlove, Stone and Storey instruct PJ to lowball – putting in his Libor estimate for the cost of borrowing dollars over 1 month at 5.30%, twenty basis points below where he thinks it should be. Dearlove tells Stone they need to get a wider audience involved and take the issue ‘upstairs’. (Dearlove, Storey and Stone - who were merely carrying out the directions of the board - have been offered the chance to comment but have not responded; Barclays declined to comment on this evidence).

Soon after the call, Storey calls Ewan to try to get the BBA to do something about lowballing, saying, ‘manipulation, for whatever reason, is going to come out.’ He also warns it would be wrong for banks to decide to raise rates together because' ‘that would be just as bad the other way round’.

Later, PJ fulminates to Barclays swaps trader Ryan Reich in New York. (Strong language alert - not for young ears):

30 November 2007

Miles Storey passes on Chris Lucas’s direction that Barclays should not be ‘outside the top end’ of other banks’ Libor submissions, meaning PJ will be posting false Libors.

4 December 07

PJ tells Dearlove that his Libor estimates are ‘a load of bollocks’ and he wants to take a stand. He writes an email for Dearlove to forward. ‘My worry is that we (both Barclays and the contributor bank panel) are being seen to be contributing patently false rates. We are therefore being dishonest by definition...Can we discuss urgently please?” He later says the same thing to Ryan Reich in New York.

5 December 07

Jon Stone says Lucas has told him he doesn’t ‘see the benefit’ of raising Barclays’ Libor submissions to a more accurate level. Dearlove speaks to Barclays compliance director Stephen Morse. ‘I don’t think it’s fair on PJ to be setting something which he knows is wrong’.

After Dearlove raises the issue with Diamond’s lieutenant Rich Ricci, Morse discusses lowballing with the UK watchdog the Financial Services Authority (FSA).

September 2007 - May 2009

The Bank of England, New York Fed, UK Treasury, Financial Services Authority and the British Bankers Association are told repeatedly by Barclays and others Libor is too low to reflect the real cost of borrowing cash and that banks are understating Libor rates to avoid speculation they are in financial trouble. Concerns communicated from commercial banks about lowballing, trader requests, manipulation. No moves to contact the police. The FSA is firmly against launching its own investigation.

16 March 2008

After running out of cash, Bear Steans is forced by a run on the bank to sell itself to JP Morgan Chase at a fire-sale price of $2 per share, with the Federal Reserve in support. Market in renewed turmoil.

9 April 2008

After complaints from banks not on the panel of Libor contributors, FSA Market Conditions Meeting discusses disconnect between US dollar Libor and cash rates. An FSA supervisor emails colleagues, ‘[the director of the banking sector - Tom Huertas] advised that the BBA will be coming in this afternoon and we will pass on our concerns that USD Libor may be subject to “manipulation”. Official sends note saying concerns have been recognised and escalated. However, an FSA internal audit team investigating this in 2013 (see p. 43, Communication 32 of this report) finds no record of this meeting.

Angela Knight sends memo, originally drafted by John Ewan, to board of BBA outlining lowballing and recommending that the BBA’s board members orchestrate ‘co-ordinated action’, directed ‘from the most senior level’ to raise dollar Libor so it more accurately reflects the interest rates at which cash is changing hands on the money markets.

{kind=link}

{kind=link}

10 April 08

Bank of England cuts interest rates. But press reports some lenders are raising them.

11 April 08

Colin Bermingham tells NY Fed’s Fabiola Ravazzolo that Barclays is not posting ‘an honest Libor’ in dollars, outlines how if you put your head above the parapet (posting higher, more accurate rates) you get bad press, so banks stay within the pack (lowballing). Fed reports it to US Treasury. A transcript of the call is released in July 2012 after Barclays Legal has redacted Bermingham’s name.

15 April 08

NY Fed speaks to BBA about lowballing. UK prime minister Gordon Brown urges banks to pass on rate cut. Media reports that ‘the price banks charge each other to lend money – known as Libor – remained stubbornly high’.

16 April 08

The Wall Street Journal publishes an exposé by Carrick Mollencamp, ‘Bankers Cast Doubt on Key Rate Amid Crisis’, alluding to banks ‘fibbing’ in their Libor rates.

BBA Board meets, chaired by HSBC global boss Stephen Green, and discusses Angela Knight’s memo. Ewan tells Miles Storey on the phone afterwards that all the board members agreed that lowballing is ‘best dealt with quietly’ and that board members should ‘have a word with the people who quote the rates’ to see if they can float the dollar Libor rate up. Storey asks Ewan what steps have been taken to avoid ‘collusion’ – ie an illegal price-fixing cartel. Ewan says they haven’t got that far. Storey suggests avoiding involving chairman and chief executives. Ewan reveals that’s who the board members are.

BBA announces that it is bringing forward its annual review of LIBOR fixings. Indicating it’s fully aware of lowballing, a Bank of England market conditions update reports: ‘the BBA asserted it could ban any member deliberately misquoting […] This was mainly thought to be aimed at European banks understating their US$ fixings, given they did not want to publicly acknowledge their higher bidding rates’.

17 April 2008

John Ewan returns call from Clive Jones of Lloyds about media reports of the BBA saying it could ban banks who misquote from the panel of Libor contributing banks. Ewan reassures Jones the BBA’s been misquoted.

Soon after his call with Ewan, Jones returns a call from Jonathan Wood of HSBC, saying HSBC is going to be raising its dollar Libor rates (its estimates of the cost of borrowing dollars over 9 and 12 months) and ‘it would be nice if somebody else would come to the party’. Jones isn’t sure; what if the BBA retract their report about removing banks from the panel? Wood says they can’t retract it because ‘I read the Board paper, mate...the BBA Board yesterday afternoon…I briefed our boss on the Board paper.’ That means Angela Knight’s memo. ‘I’ll speak to the dollar guys and then I’ll give you a callback shortly,’ says Jones.

Less than twenty minutes later, after speaking to the guys on the Lloyds dollar cash desk, Jones calls HSBC again. The phone’s picked up by a colleague of Wood’s. Jones tell him they’re not going to raise their dollar Libor estimates quite as quickly as Wood was suggesting. But they will raise them more than they were planning to before Wood called.

The same day, Miles Storey tells two FSA officials about lowballing - and the commercial reasons why Barclays is ‘guilty of being part of the pack’ (of banks that are lowballing, posting false, low estimates of the cost of borrowing dollars). , ‘We did stick our head above the parapet last year, got it shot off, and put it back down again. So, to the extent that the LIBORS have been understated, are we guilty of being a part of the pack? You could say we are. We’ve always been at the top and therefore one of the four banks that’s been eliminated. Um, so I would sort of express us maybe as not clean clean, but clean in principle.’

22 April 2008

The US watchdog the Commodity Futures Trading Commission contacts FSA staff after seeing reports of ‘possible false reporting of information to the BBA’. FSA officials discuss how they aren’t sure they have jurisdiction over Libor.

25 April 2008

BBA ‘chief executives’ meeting (governor’s advisory group) at the Bank of England, attended by John Varley of Barclays, Johnny Cameron of RBS, Nathan Bostock of Abbey National, plus senior BBA and BoE officials including Bank of England deputy governor John Gieve, Paul Tucker and future governor Andrew Bailey. Angela Knight tells them of the NY Fed’s interest in Libor. Knight confirms that BBA staff had been dispatched to the US to placate investors following the spike in dollar libors following the BBA’s intervention on 16 April. BBA later reports that ‘the BoE did not want the libor boat to be rocked when markets are so sensitive and asked what if anything could be done by them to be supportive’.

22 May 2008

Paul Tucker and others receive internal confidential memo about Libor saying, ‘Even before the money market stress, some market participants complained that Libor did not necessarily reflect where banks were actually funding. Since August 2007, this problem has become ever more severe’.

3 July 2008

In response to the BBA Libor review, Fred Sturm of the Chicago Merchantile Exchange, one of the world’s biggest users of the Libor fixings, highlights how submitters of Libor rates are choosing their answer to the Libor question, ‘At what rate could you borrow at 11am?’ from a range of accurate figures reflecting offers to lend on the money markets. He writes, ‘A Contributor Panelist who can borrow “in reasonable market size” at any one of a wide range of offered rates commits no falsehood if she bases her response to the daily Libor survey upon the lowest of these (or the highest, or any other arbitrary selection from among them).’ This evidence is later kept out of some Libor trials.

15 September 2008

US Treasury secretary Hank Paulson decides against bailing out Lehman Brothers and allows it to collapse. Markets go into a tailspin.

18 September 2008

As the crisis intensifies, Peter Johnson tells Ryan Reich, ‘I came in at five this morning and it was Armageddon […] It’s really fucking serious. Yesterday I had the Bank of England talking to me at 7.30 saying, “what’s going on?” I said, “You’ve got a real problem,” – because it really felt this morning as if someone was going to go under today. It really felt bad […] I’ve got to say, Ryan, that Libors are still fucked, mate […] the thing is, there are no offers out there.’

8 October 2008

Gordon Brown announces £50bn to recapitalise stricken banks. Six central banks (BoE, Fed, ECB, plus central banks of Canada, Sweden and Switzerland) announce co-ordinated cuts in official interest rates. Commentators say unless the real cost of borrowing down comes down – as measured by Libor and Euribor – it won’t help to ease the credit crunch.

8-13 October 2008

French banks drop Euribor submissions (estimates of the interest rates they’ll have to pay to borrow euros) by record amounts, more than after Sep 11, 2001, without any market development to justify it. Other banks in the same market don’t move at all on the same days.

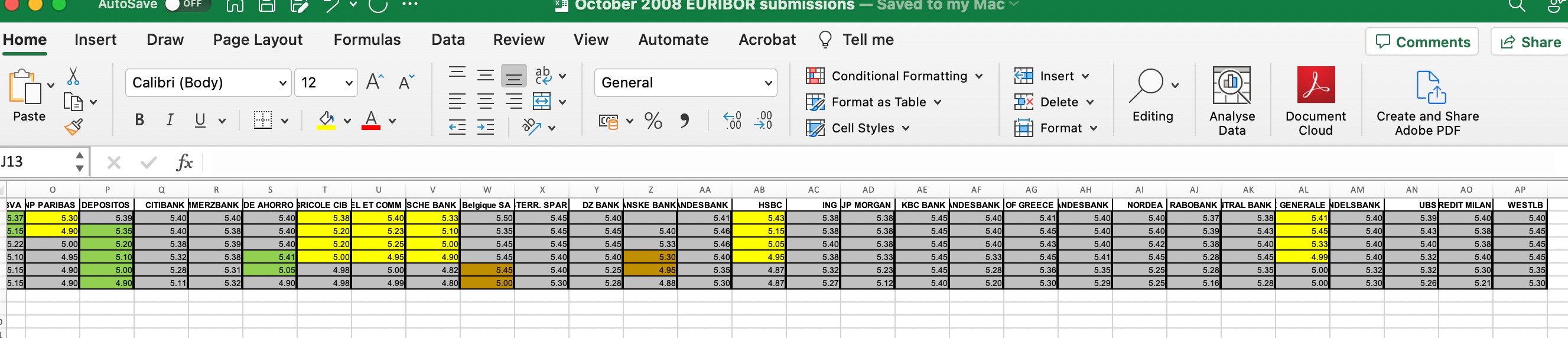

In succeeding days a) Spanish banks and b) Italian banks similarly drop their Euribor rates, some in moves of unusually round numbers eg of 10 basis points (0.10%) each day. (I can’t fit this Excel spreadsheet into one image on this page so I’m showing two overlapping screenshots; those in yellow are the French banks):

10 October 2008

At a brainstorming event with senior ECB and EU officials at Peterson Institute in Washington, ECB rates committee member Lorenzo Bini-Smaghi appeals to banks (including Deutsche, whose chief economist Tom Mayer is attending) to ‘go back to making a market’, according to email from Mayer to senior DB manager. Bundesbank gives similar message to DB’s Frankfurt office.

‘I have been informed that we do all in our power in Germany to revive the money markets. To this end we are calling all our major counter-parties. We hope the OIS-EURIBOR spreads to come in [ie for Euribor to come down] next week,’ writes Mayer.

This is evidence that banks were co-ordinating to bring Euribor down at the behest of the ECB. The email is forwarded on to top bosses Alan Cloete and Anshu Jain.

Saturday 11 – Sunday 12 October 2008

G7 emergency summit of finance ministers in Washington. ‘Balti weekend’ where RBS and Lloyds/HBOS are forced by govt into part-nationalisations. After Gordon Brown travels to Paris to meet Angela Merkel, Nicolas Sarkozy, EU president Jose-Manuel Barosso and ECB president Jean-Claude Trichet make public statements urging ‘co-ordinated action’.

13 October 2008

Barclays announces it will raise £6.5bn privately. Lloyds/HBOS and RBS announce they’re accepting UK government cash totally £37billion. In exchange the UK government takes equity stakes, part-nationalising them.

Achim Kraemer of Deutsche Bank and Jean-Christoph Doitteau of BNP Paribas (both on the ECB’s Money Market Contact Group) discuss how they’ve been trying to get other banks to push Euribors lower.

Doitteau: "The objective to lower the Euribor is definitely on the agenda."

Kraemer: "Yes, it looks a lot better for the right track. Did you manage to get a few other friends that agreed to push the fixing lower? In France all the big ones should go that way. We have raised it with a number of banks and had generally positive comments on it. Most were a bit more cautious, less aggressive but my feeling is that they'll quote a bit lower than they would have done otherwise."

"Good."

"How about the French market, any feeling?"

"Let's hope that the move will help to bring more and more banks to help it go lower."

"Agreed."

[...]"As I told you a few other big ones here agreed to move them lower. We tried to push that but the stone is heavy."

14 October 2008

After hearing rumours that the ECB’s telling other banks to put in lower Euribor rates, Barclays trader Colin Bermingham calls senior ECB official Ralph Weidenfeller to see if it’s true. Weidenfeller says he won’t tell him to do so but says he ‘can also probably not exclude that someone else might do so’.

16 October 2008

CFTC writes to FSA asking it to get information from the BBA about Libor.

Mid-October 2008

Paul Tucker calls Mark Dearlove to the Bank of England, saying Barclays’ Libor rate should be ‘put down’ because it was receiving attention from ‘the West’ (City-speak for the Westminster government). Dearlove ignores it.

21 October 2008

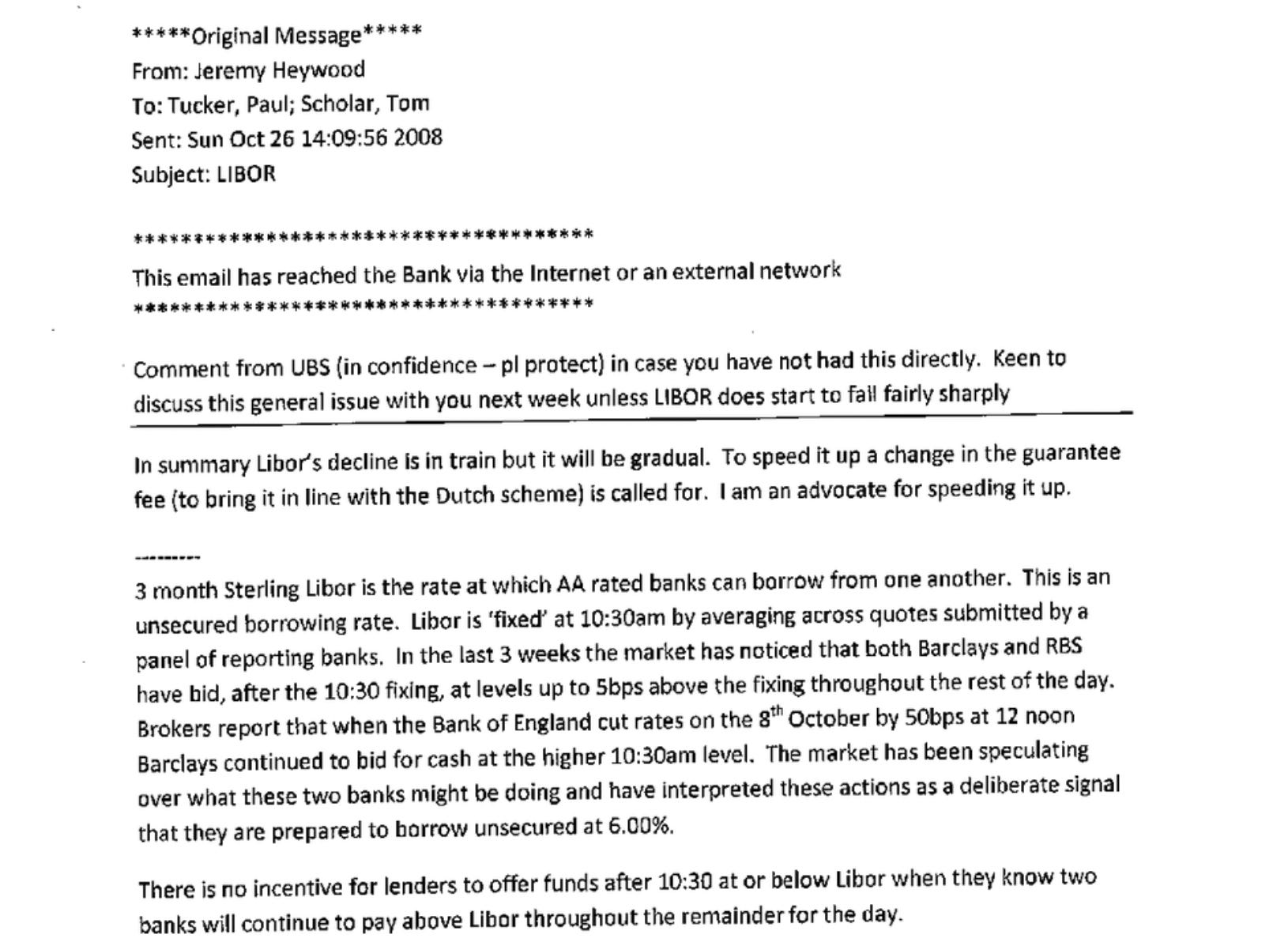

Sir Jeremy Heywood, Gordon Brown’s chief of staff at 10 Downing Street, emails Paul Tucker: ‘Why are UK LIBOR spreads not falling as fast as US?’

22 October 2008

Tucker emails Diamond and Varley; he later speaks to Diamond re Barclays’ Libor rates and mentions concern about what senior Whitehall figures are thinking. Barclays cash traders tell their bosses they’re trying to set Libor closer to the interest rates where cash is being offered; other banks are lowballing.

23 October 2008

When no-one else is lending, JP Morgan Chase New York suddenly offers to lend dollars (as Peter Johnson later tells investigators from the FBI, CFTC, SEC and FSA in an interview on 17/11/10). Brokers believe the New York Fed has urged it to do so.

24 October 2008

Barclays’ Peter Johnson speaks to New York Fed official and warns her 3-month dollar Libor rates are ‘absolute rubbish’ – around a percentage point lower than the interest rates where cash is really changing hands.

25-28 October 2008

Heywood repeatedly emails Paul Tucker, Tom Scholar (HM Treasury) exploring how to speed up falls in Libor, concerned about Barclays’ higher Libor rates.

27 October 2008

Peter Johnson again speaks to NY Fed, guides official to the page on Bloomberg that proves dollar Libors are too low. (A transcript is released in July 2012 with Johnson’s name redacted).

29 October 2008 c3pm

Tucker calls Diamond to again relay concerns of senior Whitehall figures about Barclays’ higher Libor rates. Diamond asks Tucker to tell them other banks are posting below where cash is trading; Tucker declines. Diamond dictates a file note saying Tucker told him, ‘while he was certain we did not need advice, that it did not always need to be the case that we appeared as high as we have recently.’

Worried the government might nationalise Barclays, Diamond calls Jerry del Missier and gives him an instruction that Barclays should not be outliers (ie standing out above the pack of other banks contributing to Libor). In other words, its Libors should come down (regardless of the interest rates offered by lenders in the money markets).

Del Missier passes it on to Dearlove, who calls sterling cash trader Pete Spence then calls Johnson at 3.38pm and reluctantly instructs him to lower his Libors while acknowledging it’s the ‘wrong thing to do’:

Johnson is still in shock a few minutes later when he tells a colleague about it, adding ‘no-one is meant to know’:

These calls, like others relating to the lowballing ordered from the top of the financial system, are never played to the juries in traders’ trials.

4 November 2008

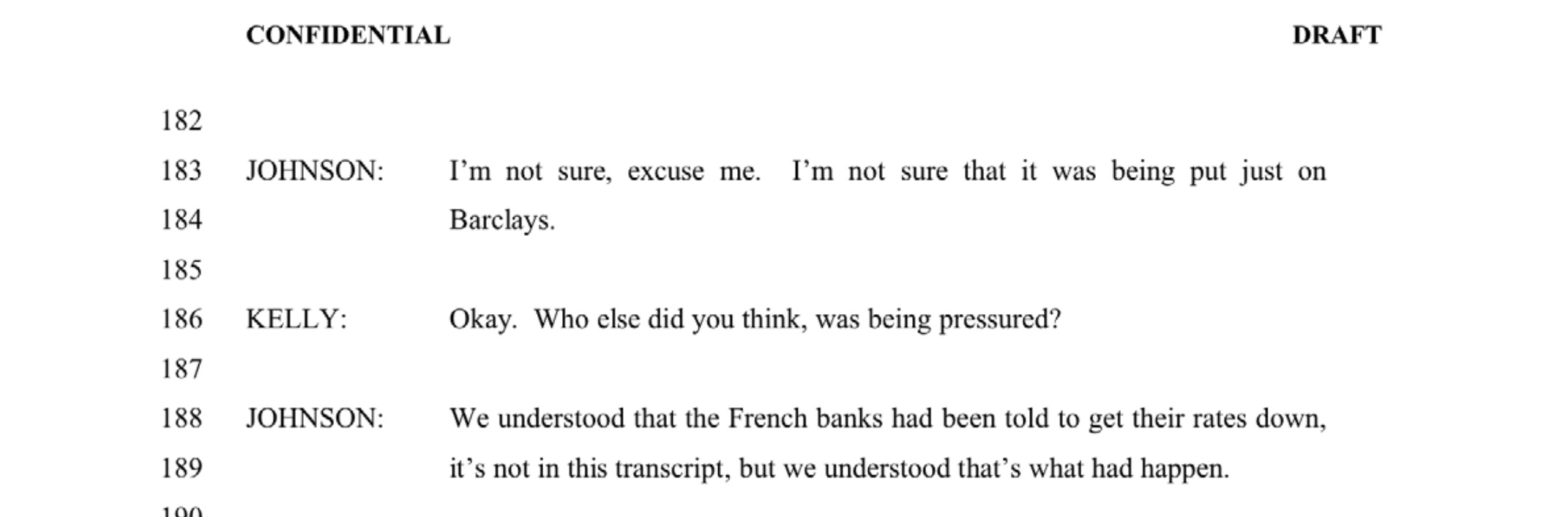

Barclays executives Jon Stone and Mark Dearlove tell top Bank of England officials there had been political pressure for French banks to cut their Euribor fixes (p. 13 of this leaked BoE market intelligence report).

5 November 2008

John Fingleton, director of the Office of Fair Trading tells FSA chief executive Hector Sants he’s ‘contemplating looking at…Libor’. They agree FSA will respond.

6 November 2008

At a meeting at Barclays Capital’s GQ, Jerry del Missier tells Barclays executives John Porter and Mark Dearlove, and senior cash traders Pete Spence, Colin Bermingham and Peter Johnson, that due to pressure from the Bank of England, submitters were to lower their Libor submissions.

Bank of England cuts official rates by 1.5%, ECB by 0.5%.

Dearlove later discusses with group chief executive John Varley how the pressure to lowball sterling Libor has been coming from Downing Street, according to a conversation Varley had with Paul Tucker.

10 November 2008

FSA staff in banking sector exchange emails about the OFT’s inquiry. ‘We would not be keen on an OFT investigation at the present time…the BBA has itself recently conducted a review of the Libor process and made some changes’; ‘More importantly, the OFT would need to be very careful about the market (and political) implications of a decision to investigate LIBOR at the present time’. Comments forwarded to office of Hector Sants the next day (see page 80, Communication 65 of this report).

18 November 2008

In unminuted comments ahead of a meeting in Frankfurt of the Money Market Contact Group, Paul Mercier of the European Central Bank tells commercial banks the ECB has played its part giving assistance to the market, according to a source present at the meeting. Mercier says it’s now time for banks to be ‘strong’ and ‘get your Euribor rates down’. (The ECB has been asked specifically about this but declined to comment).

November 2008 - March 2009

Commercial banks continue to feel under pressure from central banks to keep Libor and Euribor artificially low ie lower than the real cost of cash on the market.

9 December 2008

John Ewan meets two FSA officials to discuss CFTC’s interest in Libor and reports. He reports back to the BBA that they don’t think it has jurisdiction and see no reason for an investigation of their own.

12 January 2009

Hector Sants writes to OFT saying ‘the FSA would not encourage a further investigation as the BBA has recently conducted its own review of the process and made some changes…More importantly, we believe there may be financial stability implications of announcing an investigation at the present time, due to the Libor-OIS spread being such a key indicator of funding costs.’ This ends correspondence between FSA and OFT about Libor.

2009 to 2011

Beleiving the bank has a good record on Libor, Barclays executives agree to fund ‘Project Bruce’, an expensive trawl of its records on Libor to meet the CFTC’s requests.

February 2009

BBA writes to CFTC suggesting its investigation into Libor manipulation is misguided. The BBA is seeking legal advice on whether it needs to forward any documents to investigators. The letter is approved by the FSA before sending.

Summer 2009

Peter Johnson and Jonathan Mathew are interviewed by compliance officers and Barclays’ external lawyers, McDermott Will & Emery, appointed to oversee the bank’s response to the CFTC’s investigation. Questions focus on the crisis.

22 June 2009

New CFTC chief executive Gary Gensler revives the watchdog’s interest in Libor having seen a Financial Times article by Izabella Kaminska, ‘Libor is useless’.

30 September 2009

Interviewed by phone about trader requests by compliance officials and Barclays’ external US lawyers McDermott Will & Emery, Jonathan Mathew at first says trader requests didn’t affect settings. Towards the end, they ask about two trader request emails and Mathew tells them he may have adjusted his US Libor submission in response to them. They appear shocked, ending the interview immediately.

4-7 October 2009

CFTC acting head of enforcement Steve Obie travels to a conference in central London. He meets his friend and former colleague Greg Mocek - former CFTC head of enforcement, now at McDermott Will & Emery - at the Grosvenor House hotel, Park Lane. Mocek tells him they have found emails and messages that seem to confirm suspicions that Libor is being routinely gamed: derivatives traders putting pressure on colleagues in London to change their submissions to suit trading positions. According to the 2016 book The Fix by Liam Vaughan and Gavin Finch, Mocek has convinced himself this is ‘a whole new category of malfeasance’.

January 2010

Mocek, former CFTC head of enforcement, tells former colleagues in a presentation at their Washington offices that Barclays had been ‘shocked to identify some rogue elements’ and would ‘deal with them without mercy.’

April 2010

After coming across the PJ and Pete Spence emails of 29 October 2008, Project Bruce investigators start listening to PJ’s line. They discover the Dearlove-PJ conversation of 29 October 2008. A CD containing the audio recording is sent to CFTC officials, who share it with the US Department of Justice.

Greg Mocek and Mark Harding, general counsel of Barclays, meet FSA director of enforcement Margaret Cole. Mocek plays her the audio recording. The FSA does not investigate the evidence implicating the Bank of England and UK government in Libor manipulation.

26 April 2010

Prompted largely by the Dearlove-PJ audio recording, the United States Department of Justice launches a criminal investigation.

June 2010

Barclays Legal takes over from Barclays’ compliance department to take the lead on the Libor investigation. Peter Johnson and Jonathan Mathew are told there’s going to be a further interview with the US govt.

August 2010

Jon Mathew and Peter Johnson are interviewed by Barclays’ new lawyers Sullivan & Cromwell ahead of their interview with the US Department of Justice. Most questions are about lowballing: only a few concern derivatives’ traders’ requests. Both Jon and PJ say they only paid ‘lip service’ to the requests.

6 September 2010

At Citigroup’s offices in Tokyo, Tom Hayes is sacked in connection with Libor - a fact his trader colleagues struggle to believe.

18 November 2010

Jon Mathew is interviewed at Canary Wharf by the FBI, CFTC, FSA and Securities and Exchange Commission (SEC, the main US financial watchdog). Most questions are about lowballing. He lies about derivatives traders’ requests, saying he only paid them ‘lip service’ following instructions from his boss, PJ. Later his place at the table is taken by PJ.

19 November 2010

PJ’s interview with the FBI, CFTC, FSA and SEC continues. He tells them his instructions to lowball (to falsely understate the cost of borrowing dollars) are coming from the board of Barclays, including Chris Lucas. Asked about traders’ requests, he claims he ‘fobbed them off’ but fails to convince FBI agent Mike Kelly. They end the interview at 4.30pm.

At 5.26pm, the FSA, CFTC, SEC and DOJ recommence the interview to ask about state-led involvement in Libor rigging. PJ tells them, ‘I was effectively being told by the Bank of England to put my rates down’ and names Paul Tucker. Kelly asks him about a transcript of his call with Dearlove on 29 October 2008 and pressure being put on Barclays from on high.

PJ tells them what he’s heard from his colleague and fellow whistleblower Colin Bermingham about the European Central Bank:

PJ also refers to rumours that the Federal Reserve Bank of New York had intervened:

The evidence Johnson gives is backed up by published data on Libor and Euribor submissions from the time.

16 December 2010

Jon Mathew is interviewed by his banks’ external lawyers, who note the inconsistency between his recent evidence and the interview in September 2009 where he acknowledged he may have taken trader requests into account. Then he’s confronted with a calendar entry where he’d reminded himself to adjust a Libor submission. As he would later say on the witness stand, ‘You can’t justify setting a calendar entry to remind himself to ignore an email request.’

April 2011

The DOJ reaches out to Mathew’s lawyers, saying they believe he’s been lying. He could face a charge of obstruction of justice. If he agrees to tell ‘the truth and nothing but the truth’ (ie go along with the US Department of Justice’s version of events) then it could lead to a non-prosecution agreement.

July 2011

Jonathan Mathew and Peter Johnson are both put on gardening leave after Barclays finds out Mathew has been offered a Proffer Agreement by the US DOJ. After 30 years of service, PJ’s career at Barclays is over.

3 August 2011

Jon Mathew gives a ‘proffer’ interview at DOJ headquarters at 950 Pennsylvania Avenue, Washington. He says he knowingly made false statements regarding his accommodation of swaps traders' requests during his interviews with the banks’ lawyers and the US authorities. He says he did accommodate them.

1 November 2011

After a ‘dark period’ of nearly three months of anxiety lest he be extradited to the United States, Jon is offered a non-prosecution agreement.

November 2011 - June 2012

Detailed, complicated negotiations between Barclays Legal, the US regulators the CFTC, DOJ, SEC and FSA to agree the ‘settlement’ (meaning the level of fines and the detailed misconduct the bank will publicly acknowledge). Bob Diamond’s lieutenant Rich Ricci oversees, assisted by Barclays Capital’s top lawyer Judith Shepherd.

27 June 2012

The United States Department of Justice, the Commodity Futures Trading Commission and the UK’s Financial Services Authority announce their settlement with Barclays, imposing then-record fines totalling £290m ($450m) and publishing press releases and detailed statements of fact. Traders’ requests for adjustments to Libor estimates are treated as just as bad, or worse than, lowballing - even though the authorities will never show any false statements were made in connection with them.

‘For this illegal conduct, Barclays is paying a significant price,’ says a quote in the press release from Assistant Attorney General Lanny A. Breuer of the Justice Department’s Criminal Division - without referring to any laws that have been broken in the United States or United Kingdom. A US appeal court will later rule (January 2022) that in fact, traders broke no laws nor rules.

The DOJ’s detailed statement of fact makes no mention of the evidence the DOJ has been given of UK government involvement, nor or of the fact that the pressure on PJ to lie was coming from the 31st floor of Barclays - the top of the bank - nor of the evidence of other central banks being involved from the ECB to Banque de France to the Fed. Almost all the evidence the DOJ has been given about state-led, central bank involvement in Libor rigging is kept out of its statement of facts - leaving Congress, Parliament, the media and the public in the dark.

Nevertheless the press releases offer something the media and public have been longing for: bankers at last being fined for doing bad things. After bank bosses were left unpunished for the disastrous mismanagement of their banks that led to the 2008 banking crisis and hugely expensive government bailouts, the regulators are now issuing record fines to a bank for doing something ‘illegal’. The scandal bursts onto the news, igniting a powder keg of suppressed public anger.

3 July 2012

After days of angry criticism in the media and informal pressure from the Bank of England and FSA, Bob Diamond agrees to resign. The same day, Barclays releases details of a file note he’d dictated following a phone call on 29 October 2008 with the Bank of England’s Paul Tucker, which appears to implicate the central bank in the very same misconduct for which Barclays has just been fined.

4 July 2012

Bob Diamond appears before MPs. He begins by blaming unnamed traders for damaging Barclays through their ‘reprehensible’ actions, which he says should be dealt with ‘harshly’.

Following his comments, the story spins away from Diamond, the Bank of England and others. Pressed on when he first knew about lowballing, he claims he first knew about it ‘this month’ ie July 2012.

6 July 2012

Having said the previous week that he’d need a month to work out if he could prosecute the traders, Serious Fraud Office director David Green announces, two days after Bob Diamond’s appearance, that he’s accepted Libor for investigation.

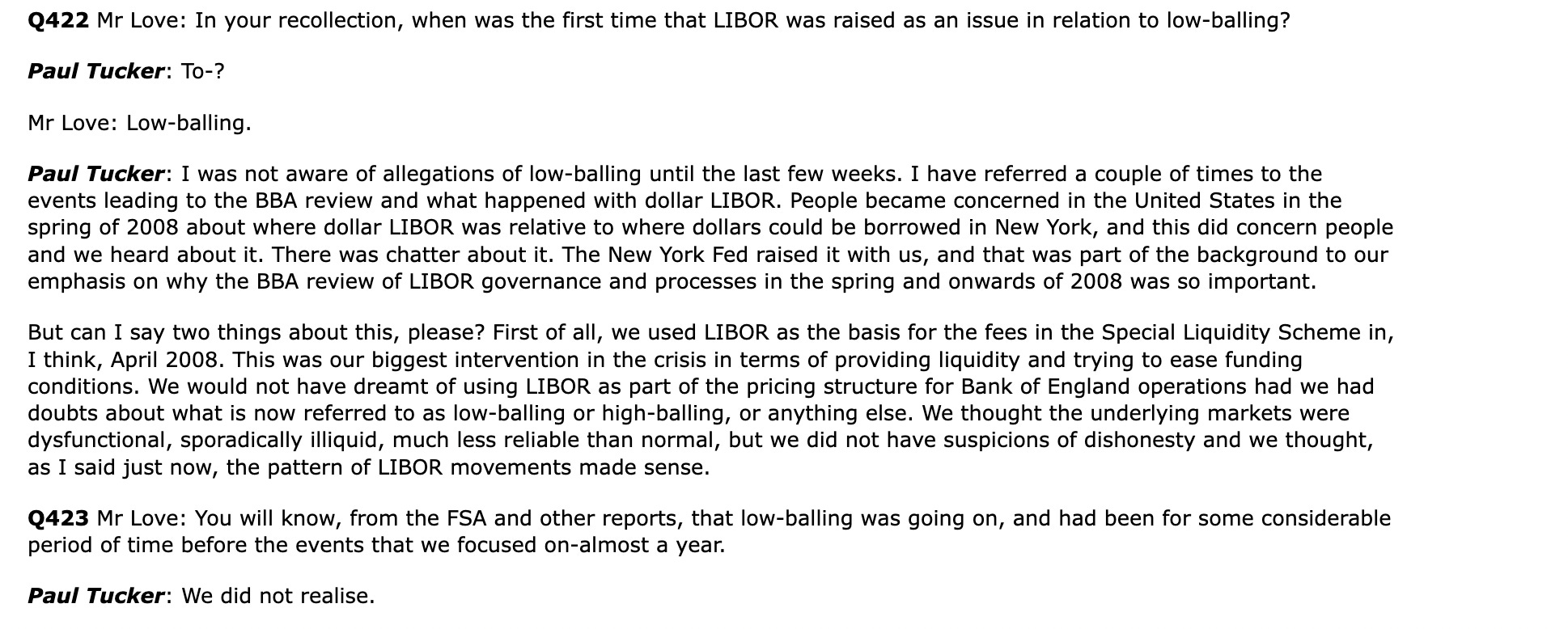

9 July 2012

Paul Tucker appears before the Treasury committee. At 17.51.48, when Andy Love MP asks him when he first knew about lowballing, he says, ‘I wasn’t aware of allegations of lowballing until the last few weeks.’

16 July 2012

Jerry del Missier appears before the Treasury committee, where he contradicts the official story (negotiated between the US regulators, the FSA and Barclays Legal) that the events of 29 October 2008 were all down to a ‘misunderstanding’, in which Diamond didn’t think he was getting an instruction from Paul Tucker, and didn’t think he was passing on an instruction to del Missier; del Missier apparently got the wrong idea. Del Missier is quite clear (question 856) that it was an instruction.

17 July 2012

The then governor of the Bank of England Sir Mervyn King appears before the committee alongside then FSA chair Adair Turner, Paul Tucker and others. King tells MPs, ‘we have been through all our records. There is no evidence of wrongdoing or reporting of wrongdoing to the Bank.’ (See the transcript here for the context or view the session here).

King later adds, ‘neither did the Fed nor anyone else send us any evidence of misreporting.’ (please see this link to view the full session).

18 August 2012

The Treasury committee publishes ‘Fixing Libor: some preliminary findings’. But there will never be a full report on it. The findings of Andrew Tyrie’s committee go along with the official version of events negotiated between Barclays Legal and the US authorities, including the highly questionable story that let the Bank of England and the board of Barclays Bank off the hook.

11 December 2012

Former UBS trader Tom Hayes is awoken by loud knocking at his Surrey home. More than twenty Serious Fraud Office investigators and police officers enter his home. He’s taken to Bishopsgate police station where he’s later interviewed. On legal advice, he says ‘no comment’ to each question.

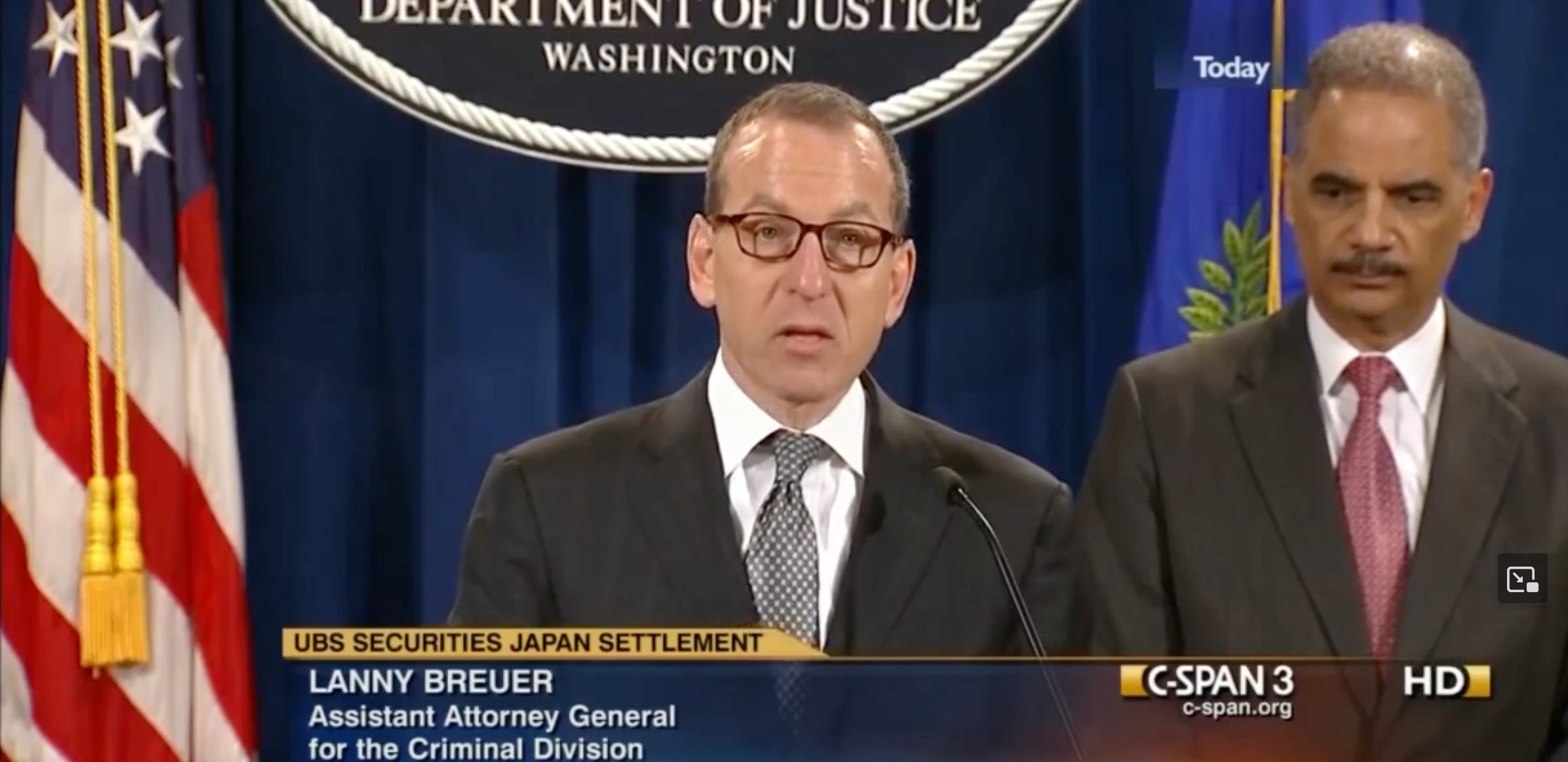

A few hours later, US Attorney General Eric Holder and the assistant attorney general in charge of the criminal division, Lanny Breuer, face a hostile reception after announcing there will be no prosecutions of HSBC bankers who had helped to launder $881m of dirty money for a Mexican drug cartel and arranged hundreds of millions of dollars of transactions in violation of sanctions against Iran and other countries. ‘It’s the case that has everything – everything except an arrest,’ says an astonished-looking CBS anchor, John Miller.

19 December 2012

UBS pays more than $1.5bn after being fined by US and UK regulators for manipulating Libor. Tom Hayes is encouraged because the press release shows his bosses knew and approved of his requests of traders to publish ‘high’ or ‘low’ Libor submissions to suit his bank’s commercial interests.

But he then watches, horrified, as he learns on live TV that he has been charged with crimes in the United States. His conduct is publicly condemned by Attorney General Eric Holder and Assistant Attorney General Lanny Breuer, with little sense of any presumption of innocence. They’re keen to show they are willing to prosecute bankers. What neither Holder nor Breuer reveal at the time is that, unlike Tom Hayes, HSBC had benefited from an unprecedented intervention by the British government, in which the then Chancellor of the Exchequer George Osborne urged the then chair of the US Federal Reserve, Ben Bernanke not to prosecute HSBC criminally, and claiming it could de-stabilise the financial system.

Advised he could spend up to 30 years in a US penitentiary, Tom Hayes is terrified of extradition. The only way to avoid is to be charged instead in the UK. He asks his lawyers to explore it. They contact the Serious Fraud Office to enter him on a programme designed for a ‘supergrass' revealing information about a drug gang or terrorist network under the Serious and Organised Crime and Police Act 2005 (SOCPA).

Note: this is a work in progress to accompany publication of Rigged. It makes no claim to be comprehensive. If you spot any errors or significant omissions then please do get in touch, either via the contact form on this blog or by DM-ing me on my Twitter account https://twitter.com/andyverity